Know Your Plan

Do you think health insurance is confusing? You’re not alone. There’s a lot to consider when you’re learning about, shopping for, and using your health insurance coverage.

Let’s Start with the Basics

What is Health Insurance?

Your health plan is an agreement between you and your insurance company.

You pay a monthly premium and some of the costs for your care.

When you get sick or hurt, your insurance company helps pay those costs.

Why Insurance is Important

Most of us can’t afford to pay out of pocket for medical care. Medical care can be really expensive and is the number one cause of bankruptcy in the United States.

Health care is expensive!

| Fusion for Back Vertebrae $117,430 |

Hip or Knee Replacement

$56,488

Back Surgery without Fusion |

| Heart Failure $16,896 |

With insurance:

- You pay a premium each month, but the cost of most health care is shared between you and your insurance company.

- You benefit because the insurance company has negotiated lower payment rates with doctors.

- The most you have to pay for care in a year is capped.

Read an overview of health insurance, including why it’s important.

Or watch the YouToons explain health insurance in this video.

How Insurance Works When You Get Sick or Injured

Key Terms To Know

Before you get started looking at health plans, there are some key terms you should know.

Premium

Your premium is the amount you pay each month for your health plan. You must pay your premium, even if you don’t get any health care services.

Deductible

Your deductible is the amount you will spend on your health care before your insurance company starts to pay some of your health care costs.

Co-insurance

Co-insurance is your share of the cost of a covered health care service. You start to pay co-insurance after you have paid your health plan’s deductible.

Health Plans

Metal Levels

Health plans through Washington Healthplanfinder come in three categories, called metal levels. They’re available in Bronze, Silver, and Gold. The difference between the plans is what percentage of the cost of care they cover (for example, Bronze plans cover 60% of the costs, where Gold covers 80%).

Essential Health Benefits

Every health plan through Washington Healthplanfinder includes 10 essential health benefits. These include:

- Doctor visits and hospital stays

- Trips to the emergency room

- Care before and after your baby is born

- Mental health and substance use treatment

- Prescription drugs

- Services and devices to help you recover if you get injured or if you have a disability or chronic condition

- Lab tests

- Preventive services including counseling, screenings, and vaccinations

- Management of a chronic disease, like diabetes or asthma

- Pediatric care

Financial Help

There are three ways to get financial assistance to help pay for the cost of insurance:

- Lower costs on monthly premiums: Premium tax credits help lower the costs of your insurance premium each month. Tax credit amounts are based on your income and other factors, like whether you have access to other affordable insurance, and are set by the federal government.

- Lower costs at the doctor’s office: Cost-sharing reductions lower the amount of health care costs you pay at the time you get health care, like going to the doctor. The amount you save depends on your income and family size. In most cases, you need to pick a Silver plan to get cost-sharing reductions.

- Free coverage: Individuals with lower incomes qualify for free coverage, called Washington Apple Health (Medicaid).

Learn more about financial help available through Washington Healthplanfinder.

Shopping for a Plan

The first thing you’ll want to do when you’re shopping for a health plan is to understand what metal level (Bronze, Silver, or Gold) might be right for you. This way, you can narrow down the plan choices. Next, make sure you’re clear about the costs of the plan, not just the premium.

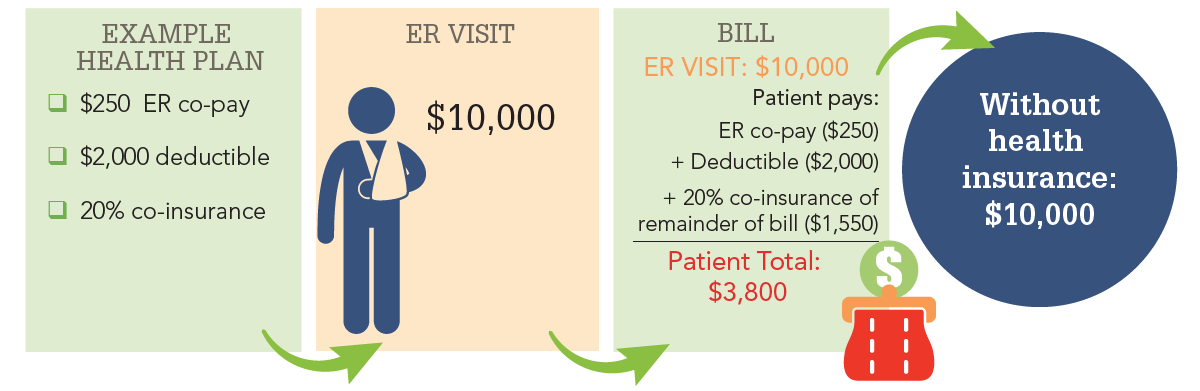

Here’s an example of insurance costs during a plan year:

- You’ll pay a premium each month for your health plan.

- At the start of the year, you pay for most of your health care until you’ve reached your deductible.

- Once you’ve met your deductible amount, you will share the cost of care with your insurance company.

- Once you’ve hit your out-of-pocket maximum, your health plan pays for all your covered services the rest of the year.

- The next year, this all starts over.

Watch this video explaining insurance costs through the year.

Summary of Benefits

A Summary of Benefits is a clear overview of a health plan’s benefits and coverage. It is a standard template so you can compare plans against each other to better understand your plan choice. On Washington Healthplanfinder, the Summary of Benefits can be found under “More information about this plan” when you’re shopping for a plan. When you pick a plan and enroll into coverage, your new health insurance company must provide a Summary of Benefits to you.

Using Your Coverage

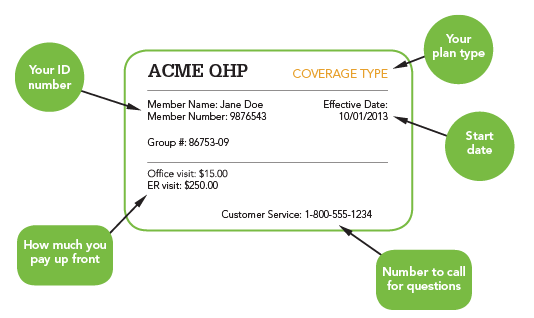

Insurance ID Card

Not all insurance cards are alike, but many insurance cards hold similar information. Your member number, coverage type, and out-of-pocket costs may be listed on the card. Bring this card with you when you go to the doctor or pharmacy.

Understanding Your Health Care Bill

After you visit the doctor, your doctor’s office sends your insurance company a claim. A claim is the way your doctor asks for payment from your insurance company, to pay for the health care services you get from the doctor. The insurance company uses that claim to pay your doctor for part of the care you received.

You might get:

- An Explanation of Benefits. This shows what services you received, what portion of the cost your health plan paid to your doctor, and if you owe the doctor any additional balance. An Explanation of Benefits is not a bill.

- A billing statement. This is a bill from your doctor’s office showing how much they are going to charge or how much they have charged your insurance company for their care.

What you need to do:

- Don’t pay any amount due until your insurance company has paid their part of the doctor’s bill.

- Make sure the dates and the care listed on the bill is right. If you have any questions about what’s listed, call your doctor’s office.

- If you have questions about what your insurance company did and didn’t pay for, call your insurance company.

- Keep this paperwork in case you might need them later.